When you play a game of Monopoly it is highly likely that you will have to pay Income Tax at some point. In this post, I’ll explain exactly what happens when you land on the Income Tax space, and what impact it can have on the game.

Income Tax Monopoly quick guide:

- The first of two Monopoly taxes in the game

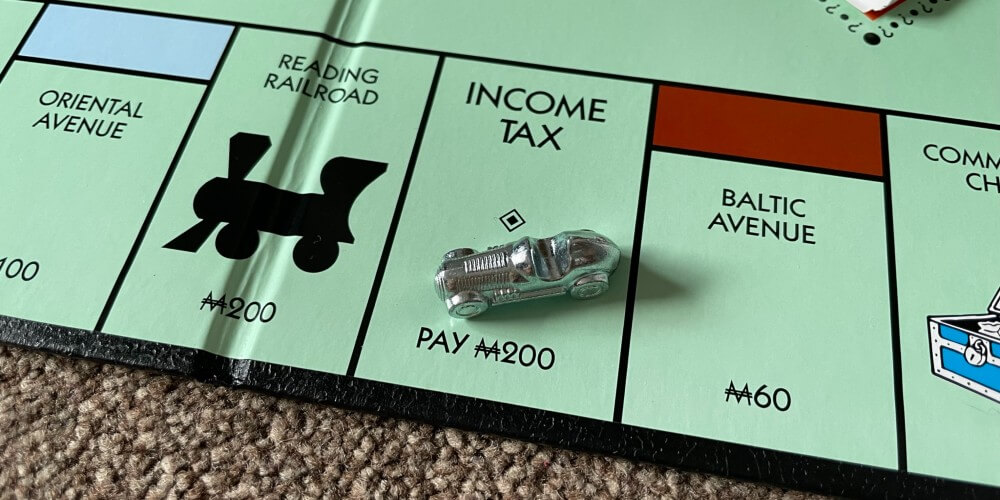

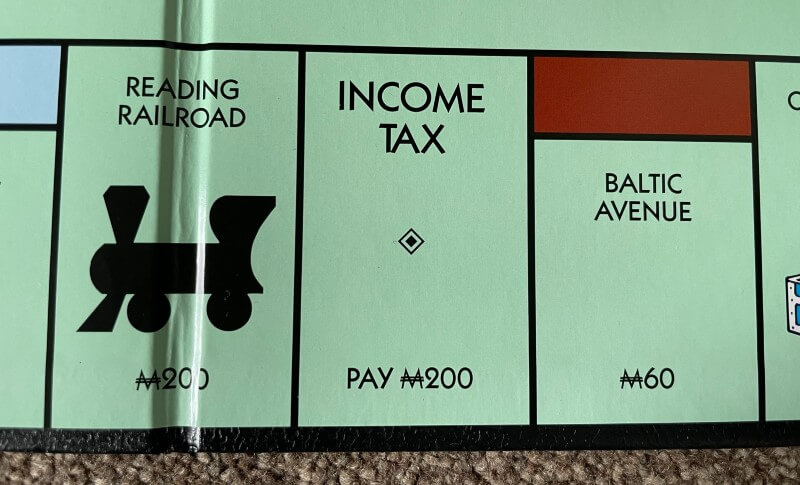

- Income Tax is the fourth space on the Monopoly board after ‘Go’

- You must pay $200 to the bank when landing on it

- Don’t put money in the middle of the board/under Free Parking. This is a house rule that slows the game down.

- Older versions of the game let you choose between paying $200 or 10% of your total assets

What Is Income Tax In Monopoly?

Income Tax is one of the two forms of taxation that are found on a Monopoly board. When a player lands on Income Tax they must immediately pay $200 to the Bank. Income Tax is the fourth space on a standard Monopoly board, nestled between Baltic Avenue and Reading Railroad.

As the square is so close to the Go space, there’s always a danger that a player will instantly lose the salary that they have been paid for passing Go (both are $200). This seems to happen to me way more often than it should!

The second type of tax in Monopoly is the Luxury Tax (known as Super Tax in the UK). This is not quite as bad as Income Tax as you only have to pay $100 if you land on Luxury Tax.

How Much Is Monopoly Income Tax?

In Monopoly, Income Tax is $200. If you land on the Income Tax space, you must immediately pay $200 to the Bank. Earlier versions of the game made before 2008 included the option to pay either $200 or 10% of your total worth.

How to calculate 10% for Income Tax

The US version of Monopoly was updated in 2008 to include the set Income Tax of $200. If you’re playing an older version of the game and have the option to choose between paying a fixed $200 fee or 10% of your total worth, you’ll need to know how to calculate this correctly.

To calculate 10% of your worth, you’ll need to add up the value of your cash, property, houses, and hotels.

To do this you add up your cash in the normal way, add the property value by using the printed price of all unmortgaged property and mortgaged value of any mortgaged properties, and finally, you add the value of your buildings by using the printed price of all your houses and hotels.

The catch is that you must say which type of tax you want to pay before adding up your net worth.

If you’re doing well and have lots of money and property then there is a risk of paying more than $200 in tax. Conversely, if you are not doing so well you will pay less income tax, which could help to stave off bankruptcy.

It is definitely easier math to use the latest version of the rules!

Interestingly, this 10% rule was never included in the UK edition which has always had an Income Tax of $200.

The very first edition of Monopoly, released in 1935, had a higher Income Tax of $300.

Where Does Income Tax Money Go?

If you land on the Income Tax space you must pay $200 to the Bank. All taxes and fines should be paid to the Bank in this way. Usually, one player is nominated as Banker and they have to make sure that taxes and fines are paid.

It is quite common for people to play using their own Monopoly House Rules, sometimes they do this without even knowing it!

One of the most popular house rules is to put all the money from fines and taxes into the middle to be won by any player that lands on the Free Parking space. This is not in the official rules! Not everyone believes me when I say this, but it’s not. Nothing happens on the Free Parking space, nothing at all.

There are also some people that use house rules that set Income Tax to always be 10%, or some other value, rather than the set $200 of modern editions.

The actual rules of Monopoly are quite finely balanced to make sure that the game is even and doesn’t go on forever, so I recommend following them to the letter. You can check out some of these lesser-known Monopoly rules to make sure you’re playing correctly.

What Happens When You Can’t Pay Income Tax?

If a player finds that they can’t pay their Income Tax during a game of Monopoly, they will be declared bankrupt and their game is over. If the player has no cash but has other assets they may still be able to avoid bankruptcy and pay the Income Tax.

If find yourself on the Income Tax space, you are obliged to pay the $200 tax. In most situations, you will pay this from your cash reserves. But, if you’re low on funds, you may still be able to pay the tax, and avoid bankruptcy, by selling some or all of your assets.

If you have any properties, they can be mortgaged at half of their face value. You can also sell houses and hotels for half of what you paid for them. You can even sell a Get Out of Jail Free card (if one of your opponents is feeling nice and buys it from you when you are on the verge of losing the game).

If you have a property that would be valuable to one of your opponents (perhaps they need it to make a set), you might be able to sell it for a higher price than mortgaging it off.

If none of this raises enough cash to pay the tax then, unfortunately, you’re out of the game and must follow the Monopoly bankruptcy rules.

To Conclude

So, that is all you need to know about Income Tax in Monopoly. No one likes to land on the Income Tax space, and it can be especially challenging if you are getting close to bankruptcy. Or super-annoying if you manage it on your first turn.

On the plus side, at least it is not quite as complicated as in real life, especially if you are using the new rules and don’t have to bother calculating the 10%.

The only percentages you’ll need to work out in modern Monopoly is when it comes to mortgage rules…